MyHassad

Unlock the chance to win valuable cash prizes and step into the world of MyHassad.

Learn more")

KFH Mobile Banking application for

smartphones with you

all the times...!

Open new account

Open new account- Transfer Money

- Open fixed deposits

- Request Credit Card

In the news..

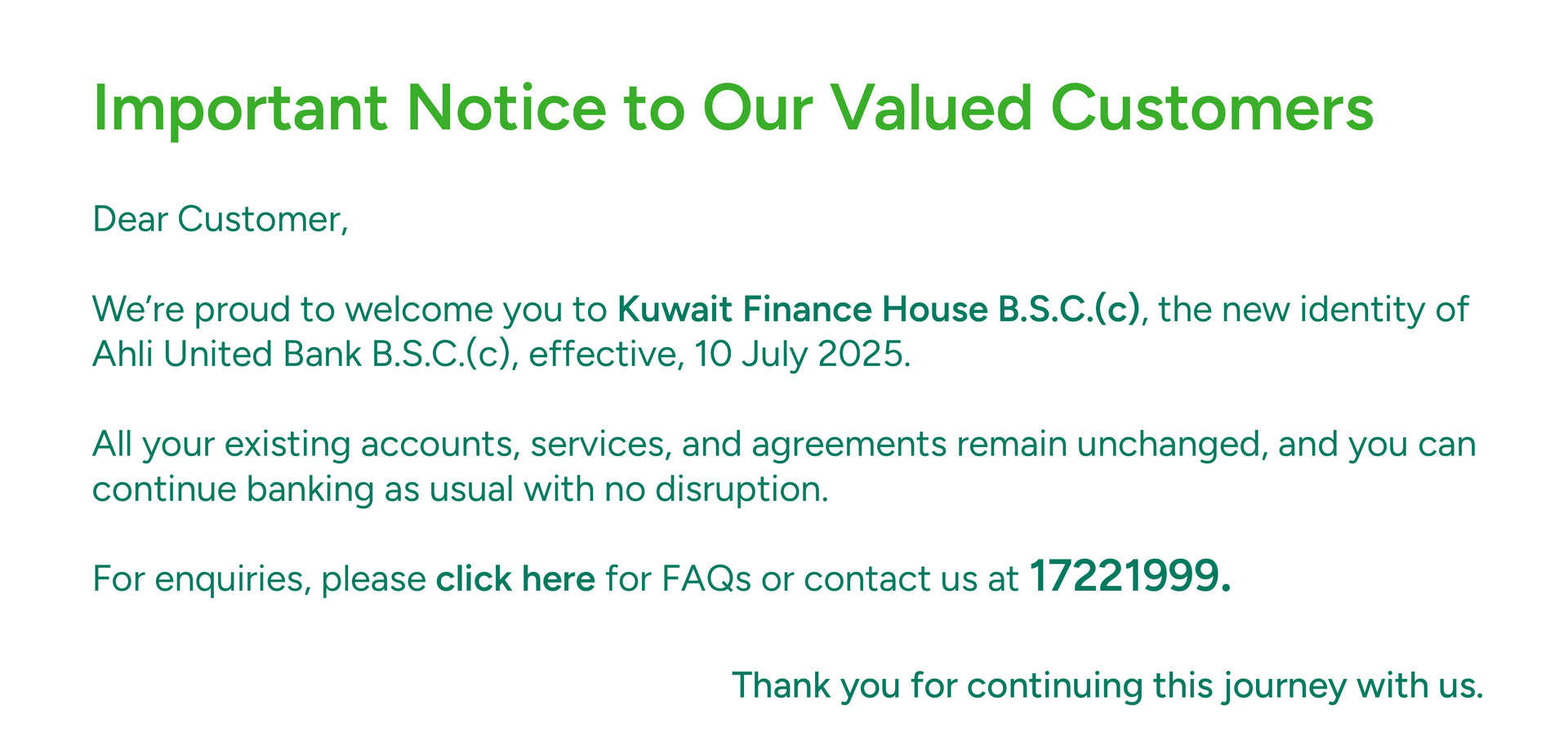

With a Strategic Vision Based on Growth, Integration, and Leadership, Ahli United Bank Announces Its New Identity as Kuwait Finance House

Manama, Kingdom of Bahrain: Ahli United Bank B.S.C. (c), a leading Islamic bank in Bahrain, has announced the start of a new chapter in its banking history under the name “Kuwait Finance House B.S.C. (c).”

Read more →

KFH announces the winners of Al-Rabeh draw

Kuwait Finance House (KFH) announced the winners of the AlRabeh draw with 20 customers...

Read more →

KFH posts strong growth with a 24% increase in nine-month net profit

KFH posts strong growth with a 24% increase in nine-month net profit, reaching AED 5.75...

Read more →